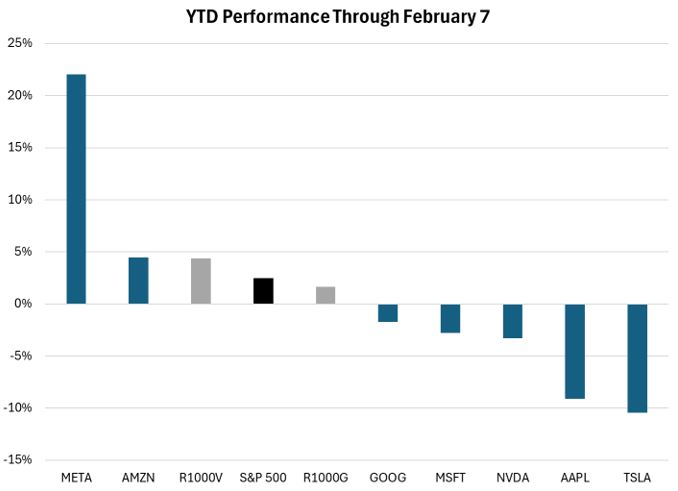

Despite a chaotic beginning to President Trump’s second term, a shocking artificial intelligence (AI) announcement from Chinese startup DeepSeek and somewhat underwhelming earnings season thus far, U.S. equities are off to a reasonably good start to 2025. The S&P 500® Index is up 4.11% as of February 14, all sectors are in the green, as are both growth and value indices. However, unlike recent years the returns of the Magnificent 7 (outside of META) are not quite ‘magnificent’ relative to broader large cap indices.

Source: FactSet® as of 2/7/2025. Please see the end for important disclosures.

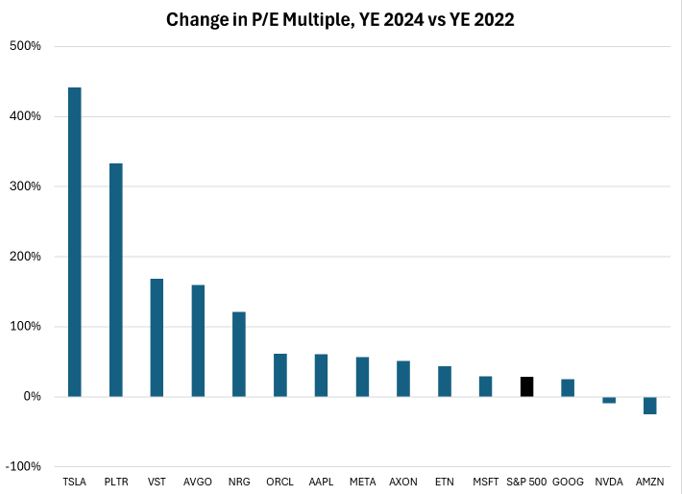

Over the past two years, there have been very few themes outside of Generative AI that allowed investors to gain access to a multi-year, high probability growth outlook. One need looks no further than the rapid acceleration in capital investment among the largest data center operators, or the parabolic revenue growth of NVIDIA (NVDA)’s data center segment to verify the optimism. In fairness, only a handful of business models have demonstrated success in monetizing this theme to date – think chip manufacturers and digital advertisers – which explains why NVDA and META have been the most magnificent stocks among the Mag 7 in recent years. Yet based on the significant P/E multiple expansion across many of the perceived Gen AI winners during 2023-24, market participants have seemingly brushed off potential risk to the longer-term growth of individual companies within this group.

Source: FactSet as of 2/7/2025. Please see the end for important disclosures.

The release of DeepSeek’s R1 model in late January created immense short-term price volatility for this group of stocks, as investors were surprised that AI reasoning and inference could potentially be accomplished at a fraction of the assumed cost and compute required. Questions as to whether hyperscalers would quickly reverse course on data center investments following the R1 revelation were struck down however as META, Google (GOOG), Amazon (AMZN) and Microsoft (MSFT) all held firm on their intentions during their January 2025 earnings calls:

META: “I continue to think that investing very heavily in CapEx and infrastructure is going to be a strategic advantage over time.”

GOOG: “We are so excited about the AI opportunity…we can drive extraordinary use cases because the cost of actually using it is going to keep coming down, which will make more use cases feasible…that’s why you’re seeing us invest to meet that moment.”

AMZN: “I believe the cost of inference will meaningfully come down. I think it will make it much easier for companies to be able to infuse all their applications with inference and with Generative AI…and we believe that this world will mostly be built on top of a cloud with the largest portion of it on Amazon Web Services.”

MSFT: “As AI becomes more efficient and accessible, we will see exponentially more demand…we have more than doubled our overall datacenter capacity in the last three years, and we have added more capacity last year than any other year in our history.”

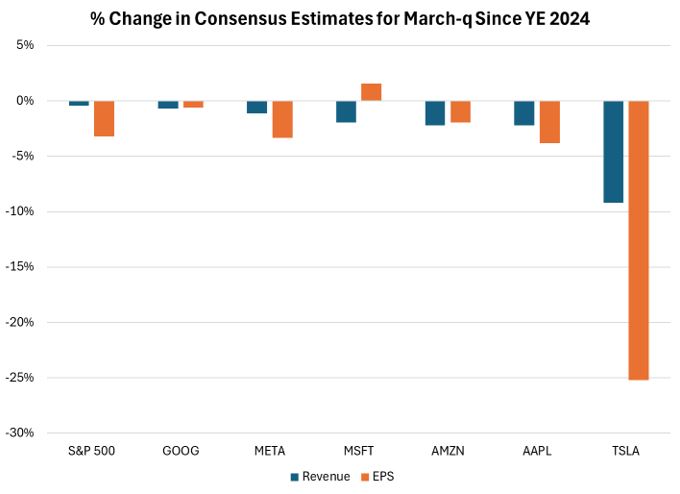

Despite this nearly unbridled optimism about the longer-term, the near-term isn’t quite as sanguine for this group. MSFT is the only member of the Mag 7 that has seen its March-quarter consensus EPS estimate rise year-to-date. All but NVDA (which has yet to report quarterly results) have seen March-quarter revenue expectations decline. A stronger dollar is largely to blame for these negative revisions, but reduced revenue and earnings expectations combined with accelerating capital expenditures is not typically a formula for stock outperformance.

Source: FactSet as of 2/7/2025. Please see the end for important disclosures.

Potentially lost in the excitement surrounding the DeepSeek R1 launch was OpenAI’s unveiling of Operator, a general-purpose AI agent that can carry out complex tasks such as planning vacations and ordering groceries without human supervision. This was soon followed by the introduction of OpenAI’s narrower agent called Deep Research that creates in-depth reports by leveraging reasoning to collate and analyze massive amounts of data with the flexibility to pivot depending on the information it discovers. Within minutes, it can produce a personalized report for a nervous parent (like me) on the best vehicle options for their new-driving teenager. AI developer Hugging Face then attempted to recreate Deep Research (which is not open-source) and within 24 hours, produced a similarly functioning agent.

These independent tools – with further polishing – may be able to save people a tremendous amount of time. Late last year, IT research firm Gartner predicted that by 2028, at least 15% of day-to-day work decisions will be made autonomously through agentic AI (up from 0%). Given the rapid pace of innovation over even just the past couple of weeks, perhaps that estimate needs to be raised. The societal implications could be wide-ranging, inclusive of job displacements, the formation of new industries and marked increases in leisure time.

Instagram, anyone?

Following two years of fairly uniform thinking, investors must consider whether the Gen AI winners of 2023-24 remain winners in 2025 and beyond. One of the potential implications of DeepSeek’s R-1 model is that large language models are in the process of becoming commoditized. As newer, faster, cheaper and most importantly, effective AI agents enter our lives, these autonomous problem-solvers may become universally available as well. Will hyperscalers be able to generate a return on their massive upfront investments in Generative AI? Will these hyperscalers slow down their pace of investment in data center infrastructure and semiconductor equipment if investors begin to lose faith – as demonstrated by a period of multiple contraction? And if so, which one blinks first?

These questions are too difficult to answer today, which is the primary takeaway here. Over just the past few weeks innovative companies in China and the U.S. have demonstrated fascinating progress in the development of Generative AI. It’s becoming more likely that complex autonomous problem solvers could become ubiquitous in society sooner rather than later. However, due to the pace of advancement, it’s less clear which companies will be outsized Gen AI winners. Beyond short-term earnings results and outlooks, this concern is likely somewhat responsible for early 2025 equity returns being good, but not quite ‘magnificent’.

Thanks for reading, and remember to never skip a Beat – Eric

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

The views expressed are solely for informational purposes and do not represent an endorsement of any political party or candidate.

Sectors are based on the Global Industry Classification Standard (GICS) sector classification system. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and Standard & Poor’s. “Global Industry Classification Standard (GICS), “GICS” and “GICS Direct” are service marks of Standard & Poor’s and MSCI. “GICS” is a trademark of MSCI and Standard & Poor’s.

The S&P 500® Index represents the large-cap segment of the U.S. equity markets and consists of approximately 500 leading companies in leading industries of the U.S. economy. Criteria evaluated include market capitalization, financial viability, liquidity, public float, sector representation and corporate structure. An index constituent must also be considered a U.S. company. These trademarks have been licensed to S&P Dow Jones Indices LLC. S&P, Dow Jones Indices LLC, Dow Jones, S&P and their respective affiliates (collectively "S&P Dow Jones Indices") do not sponsor, endorse, sell, or promote any investment fund or other investment vehicle that is offered by third parties and that seeks to provide an investment return based on the performance of any index. This document does not constitute an offer of services in jurisdictions where S&P Dow Jones Indices does not have the necessary licenses. S&P Dow Jones Indices receives compensation in connection with licensing its indices to third parties.

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected and historical growth rates. The Russell 1000® Value Index is constructed to provide a comprehensive and unbiased barometer for the large-cap value segment. The Index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect value characteristics. The Russell 1000® Value Index and Russell® are trademarks/service marks of the London Stock Exchange Group

Price-Earnings Ratio (P/E Ratio) is the ratio of the share of a company’s stock compared to its per-share earnings. P/E calculations presented use FY2 earnings estimates; FY1 estimates refer to the next unreported fiscal year, and FY2 estimates refer to the fiscal year following FY1.

Earnings per share (EPS) is calculated as a company’s profit divided by the outstanding shares of its common stock.

An investor cannot invest directly into an index.

Stocks: Alphabet (GOOG), Amazon (AMZN), Microsoft (MSFT), Eaton Corporation PLC (ETN), Vistra Corp (VST), NVIDIA (NVDA), Meta Platforms (META), Apple (AAPL), Tesla (TSLA), Axon Enterprise Inc (AXON), Oracle Corp (ORCL), NRG Energy Inc (NRG), Broadcom Inc (AVGO), and Palantir Technologies Inc (PLTR)/sub>

Magnificent Seven stocks:Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla.

Source: FactSet®. FactSet is a registered trademark of FactSet Research Systems, Inc